The "No Tax on Tips" deduction is new territory for most tax preparers. Under the OBBBA legislation, eligible workers can now deduct qualified tip income, but the documentation requirements are creating confusion across the industry.

We're seeing preparers make the same mistakes repeatedly. Here are the seven most common documentation errors and how to fix them before they become IRS problems.

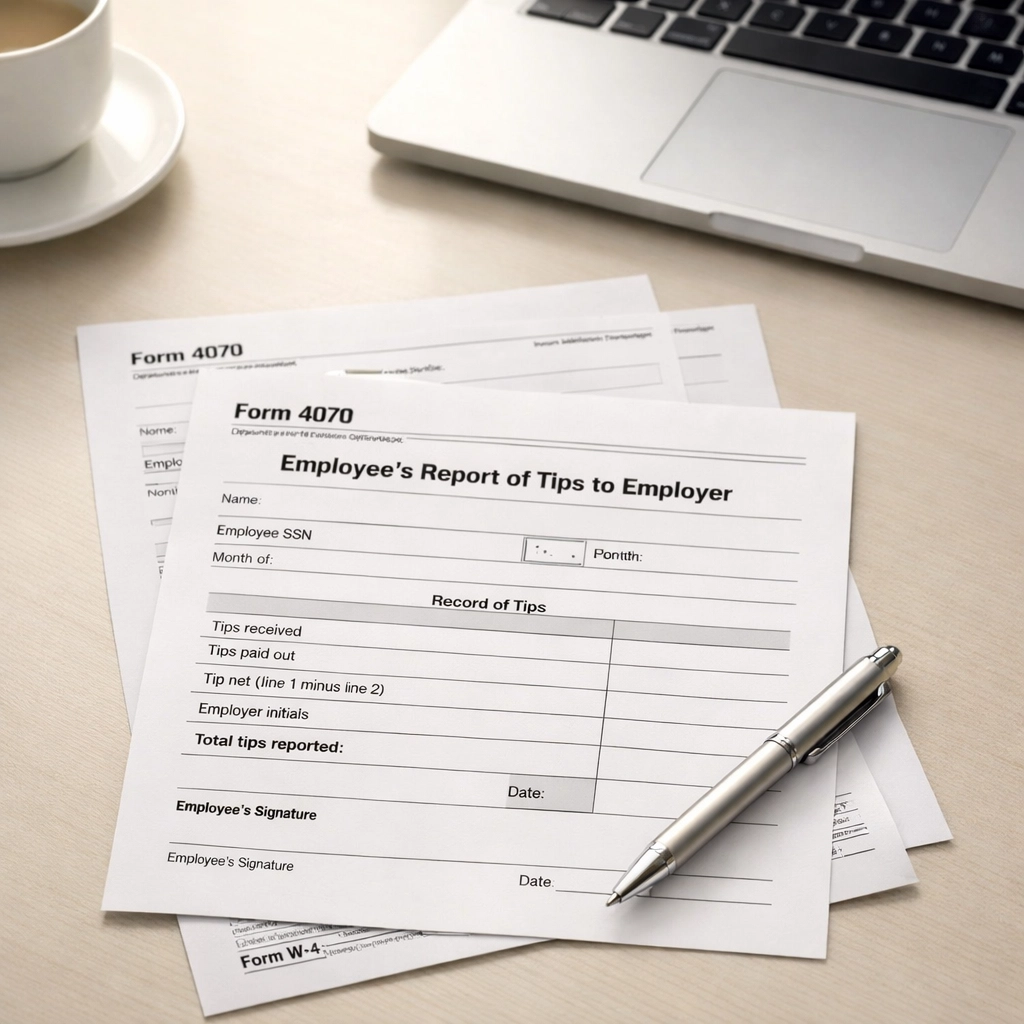

Mistake 1: Ignoring Form 4070 for 2025 Returns

The Problem: Many preparers are relying solely on W-2 data without requesting Form 4070 records.

For the 2025 tax year, employers aren't required to separately report qualified tips on Form W-2. That means the total tips shown on the W-2 likely includes both qualified and non-qualified tips mixed together.

The Fix: Request all Form 4070 (Employee's Report of Tips to Employer) records from your clients. These monthly reports create a paper trail that substantiates the tip income calculation. Have clients add up their total reported tips from all Form 4070s submitted throughout the year. This becomes your baseline for calculating the deduction.

Mistake 2: Missing the $25,000 Cap

The Problem: Preparers are applying the deduction to the full tip amount without checking the statutory limit.

The no tax on tips deduction has a maximum limit of $25,000 per taxpayer. Some preparers are overlooking this cap, especially for high-earning servers, bartenders, and hospitality workers who exceed this threshold.

The Fix: Calculate total qualified tips first, then apply the $25,000 cap. Document which tips fall within the deductible amount. For clients exceeding the cap, explain that only $25,000 is deductible regardless of total tip income. Keep notes in the client file showing you applied the cap correctly.

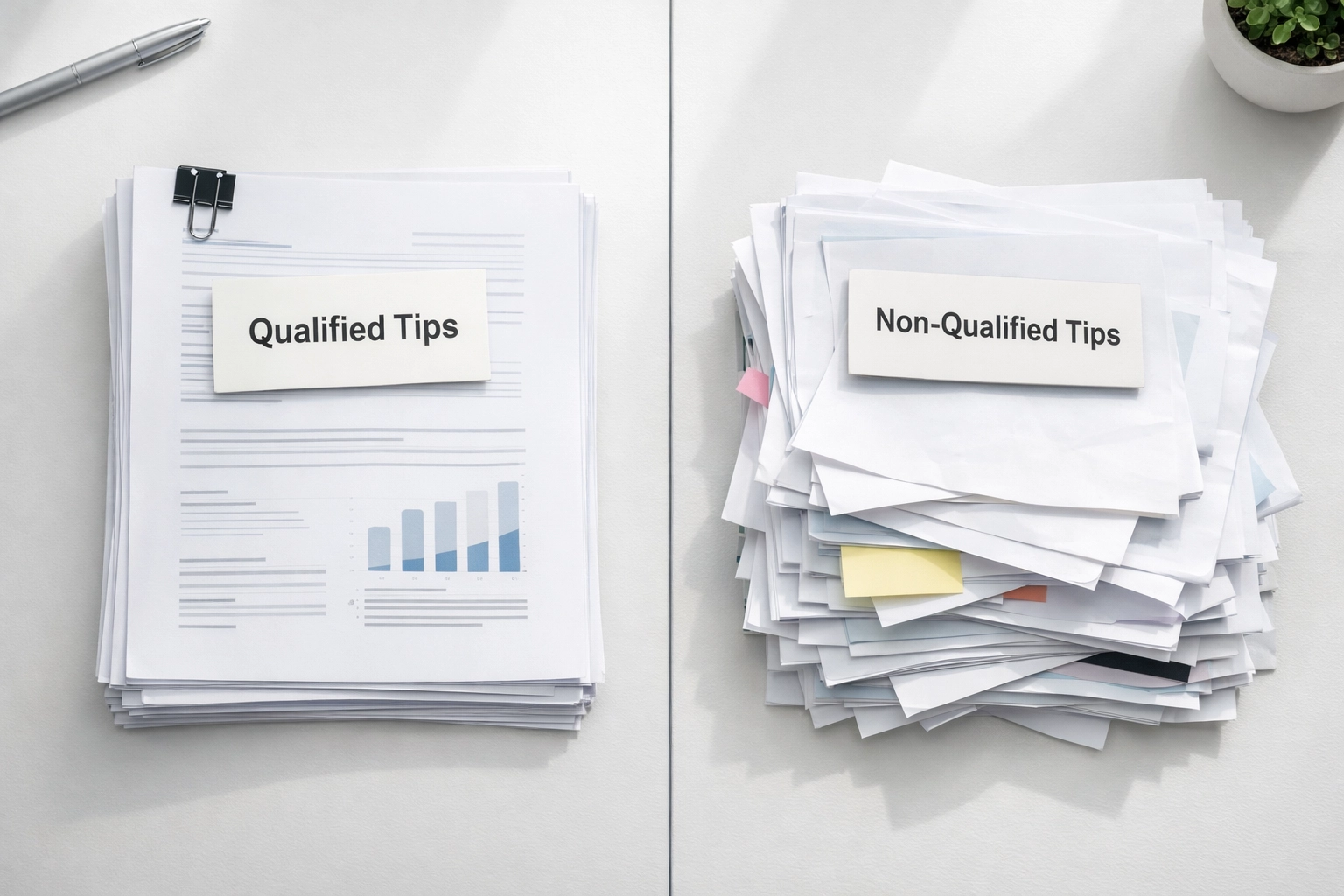

Mistake 3: Including Non-Qualified Tips in the Deduction

The Problem: Not all tips qualify for the deduction, but some preparers are treating all tip income the same.

Only tips from specific service occupations qualify. Tips from non-service roles, management positions, or certain professional services don't meet the requirements. Including ineligible tips inflates the deduction and creates audit risk.

The Fix: Verify the client's occupation code and job duties. The deduction applies to service workers in food and beverage, hospitality, personal care, and similar industries. If the client has multiple income sources or changed jobs during the year, separate qualified tips from non-qualified tips. Document the occupation verification in your work papers.

Mistake 4: Not Verifying Unreported Tips on Form 4137

The Problem: Some preparers are missing unreported tips that should be included in the deduction calculation.

Form 4137 reports tips that weren't reported to the employer during the year. These tips still count toward the no tax on tips deduction if they're otherwise qualified, but only if properly documented.

The Fix: Ask clients directly if they received tips they didn't report to their employer. If yes, they need to file Form 4137. Add these verified unreported tips to your calculation, but require supporting documentation like daily tip logs or payment records. The IRS will expect proof these tips actually existed.

Mistake 5: Failing to Maintain Daily Tip Logs

The Problem: Relying on employer records alone without client-maintained daily logs.

Employer records might not capture the full picture, especially for cash tips. Without daily logs, you have no backup documentation if the IRS questions the deduction amount.

The Fix: Implement a daily tip log requirement for all clients claiming this deduction. The log should include date, shift worked, total tips received, tip type (cash, credit card, digital), and any tip-outs to other staff. This contemporaneous record-keeping strengthens the documentation package significantly. Provide clients with a simple template they can use throughout the year.

Mistake 6: Not Preparing for 2026 Form W-2 Changes

The Problem: Treating 2025 documentation as the permanent standard.

Starting with the 2026 tax year, only qualified tips separately reported on Form W-2, 1099-NEC, 1099-MISC, 1099-K, or Form 4137 will be deductible. Employers will be required to break out qualified tips on these forms. The documentation rules are changing.

The Fix: Educate clients now about the 2026 changes. If they're self-employed or receive tips through multiple channels, explain that proper form reporting will be mandatory. For clients with employer relationships, confirm the employer understands their new reporting obligations. Document these conversations. The transition year is the time to set up proper systems.

Mistake 7: Missing 1099-K Tip Income

The Problem: Overlooking digital payment platform tips that appear on Form 1099-K.

Many service workers now receive tips through apps, payment platforms, and digital wallets. These tips generate Form 1099-K reporting. Some preparers are only looking at W-2s and missing this additional tip income that could qualify for the deduction.

The Fix: Request all 1099-K forms from clients who receive tips through digital platforms. Cross-reference amounts with the client's daily tip logs. Add qualified digital tips to your total calculation. Keep copies of all 1099-K forms in the client file. Remember, starting in 2026, only tips separately identified on the 1099-K will qualify: so track this carefully.

Documentation Checklist for Every Return

Create a standardized documentation package for every no tax on tips deduction claim:

- All Form 4070 monthly reports

- Form W-2 showing total tips

- Form 4137 if applicable

- All 1099-K, 1099-NEC, or 1099-MISC forms

- Daily tip log for the full year

- Occupation verification

- Calculation worksheet showing qualified vs. non-qualified tips

- Cap calculation showing $25,000 limit application

The Bottom Line

The no tax on tips deduction documentation requirements are strict because the IRS expects substantiation. These seven mistakes create audit risk for both you and your clients.

Fix your documentation process now. Implement standardized intake forms, create checklists, and establish clear communication with clients about record-keeping requirements.

The 2026 rule changes are coming. Preparers who master the documentation requirements this year will have smoother filing seasons ahead.

For more guidance on current tax law changes, visit TIG Tax Pros.