The gig economy created a tax reporting problem. Millions of workers now receive income through payment apps and third-party platforms. The IRS attempted to solve this with Form 1099-K reporting requirements. The result was confusion, client panic, and a massive influx of questions to tax preparers.

Tax professionals face two challenges: understanding the 1099-K rules and filing returns for clients without holding an IRS EFIN. Both problems have solutions.

The Current 1099-K Landscape

Form 1099-K reports gross payments received through third-party settlement organizations. The threshold dropped to $600 for 2024 and beyond, affecting significantly more taxpayers than previous years.

Payment processors issue 1099-K forms to anyone receiving $600 or more in business payments during the tax year. This includes:

- Rideshare drivers

- Delivery workers

- Freelance consultants

- Online sellers

- Service providers using payment apps

The form reports gross receipts only. It does not account for business expenses, refunds, or personal transfers mixed into payment accounts.

Why Clients Panic Over 1099-K Forms

Clients see a 1099-K showing $15,000 in payments and assume they owe taxes on the full amount. They do not understand that business expenses reduce taxable income. They also mix personal transfers with business income in the same payment account.

The IRS receives the same 1099-K information. If a tax return does not report matching income, the IRS generates automated notices. This creates compliance issues for taxpayers who ignore the form or report income incorrectly.

Tax preparers must educate clients on proper 1099-K handling and accurate income reporting.

Critical Client Intake Questions

Ask these questions during every gig economy client consultation:

Did you receive a 1099-K? Many clients do not understand what the form means or how to locate it in their payment app.

Do you separate personal and business payments? Most gig workers use one payment account for everything. This makes accurate reporting nearly impossible.

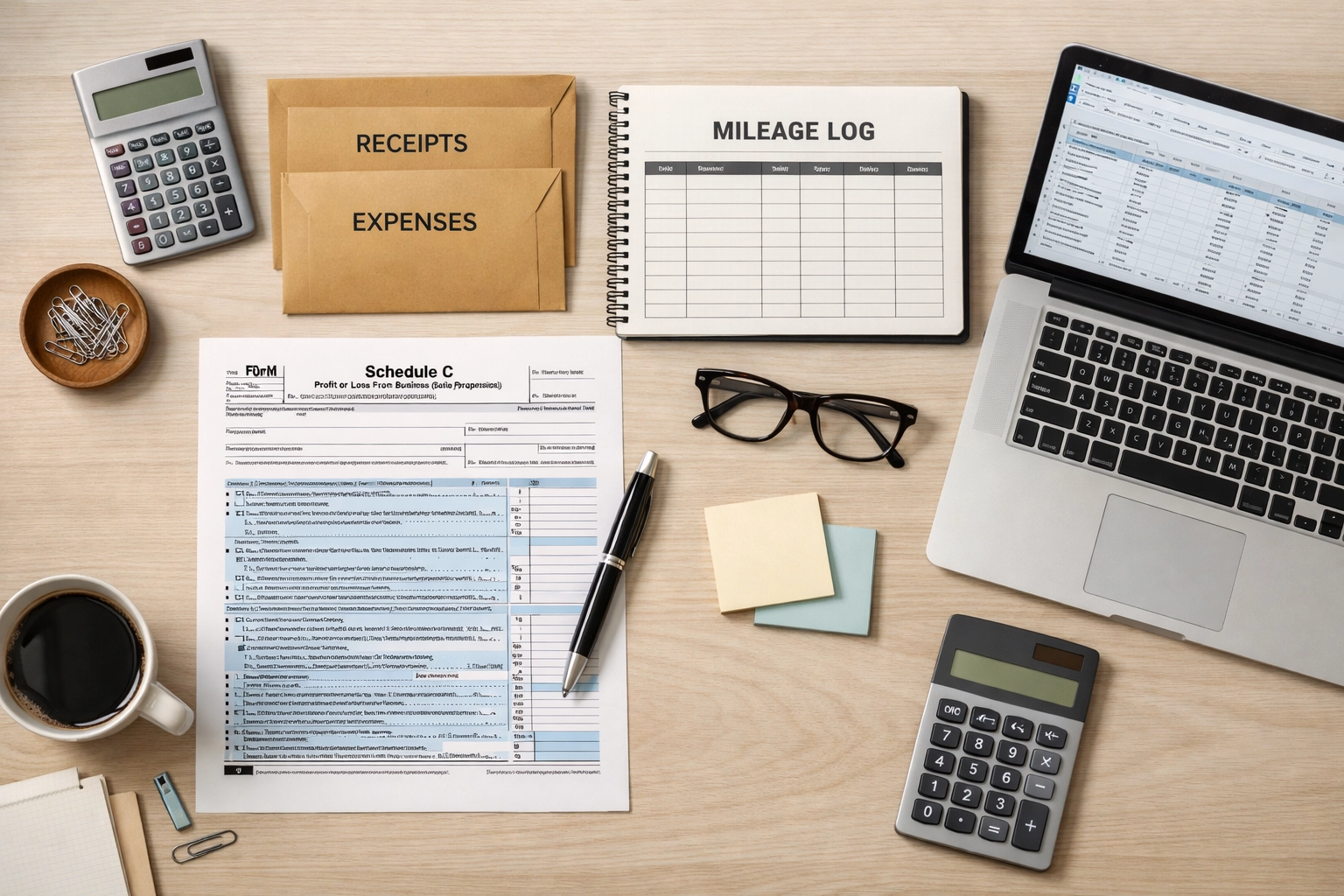

Do you track business expenses? Clients often lack receipts, mileage logs, or expense documentation.

Do you have other gig income not reported on 1099-K? Cash payments, tips, and income from platforms below the reporting threshold still require reporting.

These questions determine the scope of work needed to prepare an accurate return.

The Service Bureau Solution

Tax preparers without an IRS EFIN cannot electronically file tax returns. Obtaining an EFIN requires application approval, fingerprinting, suitability checks, and ongoing compliance obligations.

Service bureau support provides an alternative. A service bureau holds the EFIN and transmits returns on behalf of preparers. The preparer completes all tax preparation work. The service bureau handles electronic filing.

This model works for:

- New tax preparers building a client base

- Seasonal preparers without sufficient volume to justify EFIN maintenance

- Preparers who failed suitability checks

- Professionals offering tax services as an add-on to other business activities

TIG Tax Pros offers service bureau support that allows preparers to file compliant returns without holding their own EFIN. The preparer maintains the client relationship and completes all preparation work. Learn more about our services.

Proper 1099-K Reporting Process

Follow this process for every gig economy client:

Step 1: Gather All Income Documents

Collect all 1099-K forms, 1099-NEC forms, and payment records. Gig workers often receive income from multiple sources. All income is taxable regardless of whether a form was issued.

Step 2: Separate Personal Transactions

Review payment account statements. Identify and exclude personal transfers, reimbursements, loans, and gifts. Only business income is taxable.

Step 3: Calculate Gross Business Income

Total all business income from all sources. This amount goes on Schedule C, not the 1099-K amount.

Step 4: Document Business Expenses

Categorize and total ordinary and necessary business expenses. Common deductions include:

- Mileage or actual vehicle expenses

- Supplies and materials

- Equipment purchases under $2,500 (de minimis safe harbor)

- Phone and internet costs (business portion)

- Home office expenses (if qualified)

- Professional fees and subscriptions

Expenses reduce taxable income. Without documentation, the IRS disallows deductions.

Step 5: Complete Schedule C

Report business income and expenses on Schedule C (Profit or Loss From Business). Calculate net profit or loss. This amount transfers to Form 1040.

Step 6: Calculate Self-Employment Tax

Net earnings of $400 or more trigger self-employment tax liability. Calculate this on Schedule SE. Self-employment tax covers Social Security and Medicare obligations.

Step 7: Consider Estimated Tax Payments

Gig workers rarely have taxes withheld. If the client owes more than $1,000, they should make quarterly estimated payments. Advise clients to adjust withholding on W-2 jobs or submit Form 1040-ES payments.

Common Mistakes to Avoid

Reporting Gross 1099-K Amount as Income

The 1099-K shows gross receipts. Always calculate actual business income after separating personal transactions.

Forgetting Non-1099-K Income

Income below reporting thresholds still requires reporting. Cash payments, tips, and smaller platform payments are taxable.

Missing Expense Documentation

Clients often track income but ignore expenses. Require receipts, logs, and bank statements for all deductions claimed.

Overlooking Qualified Business Income Deduction

Schedule C filers may qualify for the 20% QBI deduction. This reduces taxable income further.

Ignoring State Tax Obligations

Many states have additional reporting requirements for gig economy workers. Verify state filing requirements.

Building a Gig Economy Tax Practice

The gig economy continues expanding. Workers need qualified tax preparers who understand 1099-K reporting and self-employment obligations.

Position your practice to serve this market:

- Advertise expertise in rideshare, delivery, and freelance tax preparation

- Offer mid-year consultations to help clients track income and expenses

- Provide estimated tax calculation services

- Educate clients on quarterly payment requirements

- Use service bureau support to file returns while building your practice

Technical Requirements for Preparers

Handling gig economy returns requires specific knowledge:

Schedule C Preparation

Master business income and expense categorization. Understand depreciation rules, home office deductions, and vehicle expense calculations.

Self-Employment Tax Calculations

Know how to complete Schedule SE accurately. Understand the interaction between self-employment tax and income tax.

Estimated Tax Planning

Calculate quarterly payment amounts using Form 1040-ES. Advise clients on penalty avoidance strategies.

Multi-State Issues

Gig workers often earn income in multiple states. Research nexus rules and filing requirements for each state.

When Service Bureau Support Makes Sense

Consider service bureau filing if:

- You prepare fewer than 50 returns annually

- You want to test tax preparation as a business before committing to EFIN requirements

- You failed the EFIN suitability review

- You offer tax services alongside another primary business

- You want to focus on preparation without handling filing logistics

Service bureau arrangements allow immediate entry into tax preparation. You maintain client relationships and control pricing while outsourcing the electronic filing function.

Implementation Steps

Start handling gig economy clients today:

- Review 1099-K reporting rules and Schedule C requirements

- Create a client intake questionnaire specific to gig workers

- Develop an expense tracking system for clients

- Establish a service bureau relationship if needed

- Market your services to gig economy workers in your area

The 1099-K reporting expansion created opportunity for tax preparers. Workers need guidance separating personal and business income, documenting expenses, and filing compliant returns. Tax professionals who master gig economy preparation will build sustainable practices serving this growing market.

Service bureau support removes the EFIN barrier. You can begin serving clients immediately while providing the same quality service as EFIN holders.