SEO Title: ERO Operations Framework for California Tax Preparers

Slug: ero-operations-framework-california-tax-pros

Excerpt: California tax professionals face EFIN application delays. This proven ERO operations framework enables scaling through service bureau models and streamlined processes.

Tags: ERO Operations, California Tax Preparers, EFIN, Service Bureau, Tax Business Growth, E-File Compliance

The EFIN Bottleneck

California tax preparers encounter a significant operational barrier: obtaining an Electronic Filing Identification Number (EFIN) from the IRS. The application process requires fingerprinting, background checks, and approval timelines extending 45-60 days. For new practitioners or those expanding operations, this delay halts revenue generation during peak season.

Service bureau partnerships provide immediate e-filing capability. This model eliminates EFIN dependency while maintaining full operational control.

Core ERO Operations Framework

Client Authorization Protocol

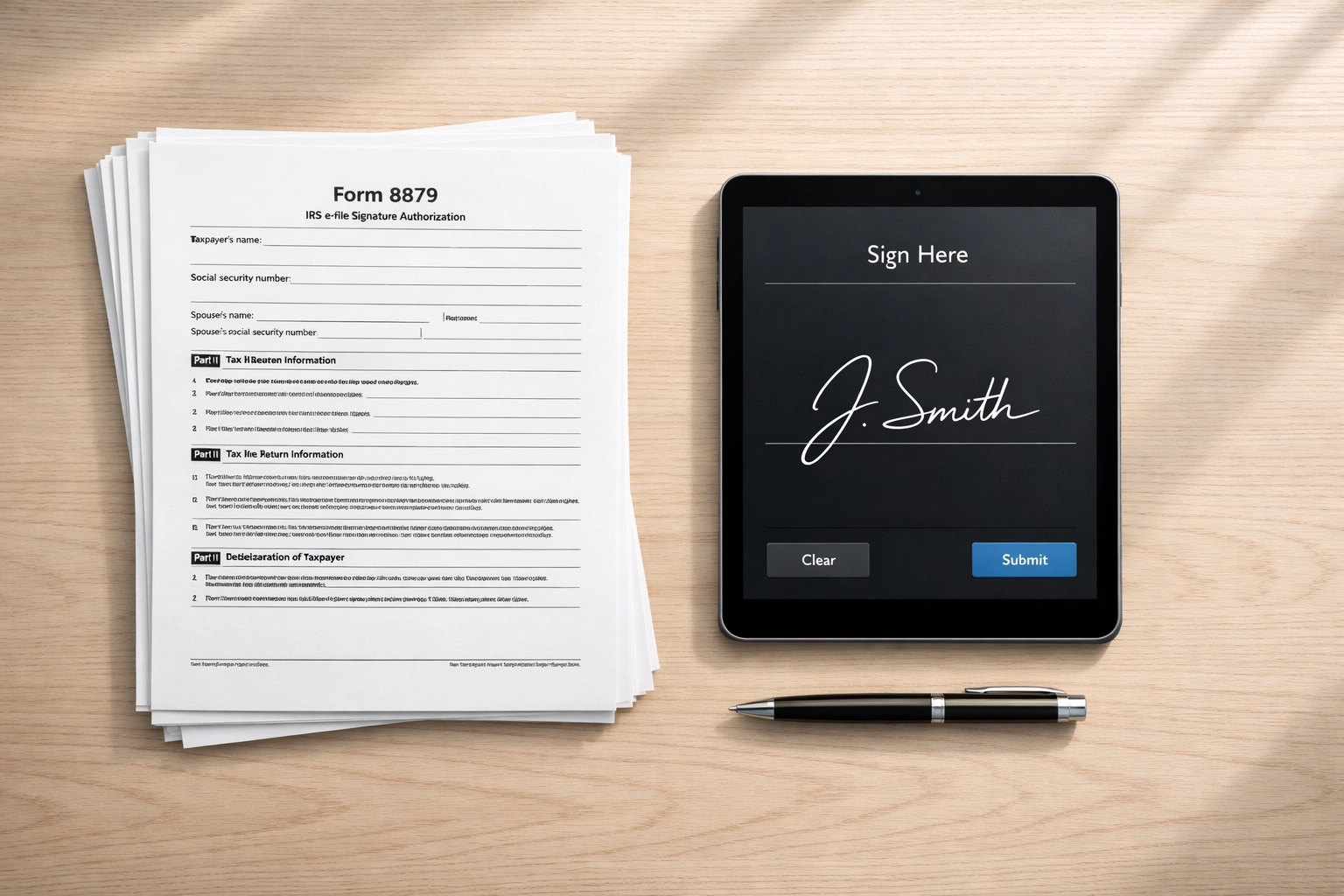

Form 8879 (IRS e-file Signature Authorization) constitutes the mandatory client authorization document. Implement these procedures:

- Collect signed Form 8879 before transmission

- Verify taxpayer identity through government-issued identification

- Document authorization date and method (in-person, electronic)

- Store authorizations for three years minimum

California practitioners must also comply with CTEC requirements for client engagement letters and fee disclosures.

Transmission Standards

EROs must transmit returns within 24 hours of receiving signed Form 8879. Service bureau models streamline this requirement:

- Upload completed returns to secure portal

- Service bureau validates data

- Transmission occurs under service bureau EFIN

- Acknowledgment returns to preparer within hours

This process maintains the 24-hour standard without managing IRS e-Services access or troubleshooting transmission errors.

Recordkeeping Requirements

IRS Publication 1345 specifies mandatory retention:

Required Documents:

- Signed Forms 8879

- Copies of all supporting documents (W-2s, 1099s, receipts)

- IRS acknowledgment files

- Due diligence documentation

- Client communication records

Retention Period: Minimum three years from return due date or IRS receipt date, whichever is later.

California practitioners operating under CTEC registration face additional state-level recordkeeping for continuing education and bond documentation.

Client Communication Framework

Establish standardized communication protocols:

- Initial Engagement: Provide written fee schedule and service scope

- Data Collection: Issue document checklist with deadlines

- Review Process: Schedule appointment for return review and signature

- Transmission Confirmation: Send acknowledgment within 24 hours

- Payment Instructions: Provide IRS Direct Pay or EFTPS guidance for amounts owed

Service bureau models simplify technical communication. Preparers focus on tax planning and client relationships rather than explaining transmission errors or software issues.

Service Bureau Model Structure

Operational Benefits

Service bureau partnerships enable immediate scaling:

- No EFIN Application: Begin operations immediately

- No Software Investment: Access professional-grade platforms

- No IRS e-Services Management: Bureau handles credentials and access

- Reduced IT Infrastructure: Cloud-based systems eliminate server requirements

- Professional Support: Technical assistance for transmission issues

Cost Analysis

Traditional ERO setup costs:

- EFIN application and fingerprinting: $150-300

- Professional tax software: $1,000-5,000 annually

- IRS e-Services troubleshooting time: 10-20 hours per season

- IT infrastructure and security: $500-2,000

Service bureau per-return fees range $5-15 depending on volume. Breakeven occurs at 200-400 returns annually. Preparers processing fewer returns save significant capital.

Quality Control Integration

Service bureaus perform automated validation before transmission:

- Error checking against IRS business rules

- SSN and EIN validation

- Mathematical accuracy verification

- Form completion requirements

This pre-transmission review reduces rejection rates from 8-12% to under 2%.

Implementation Process

Phase 1: Service Bureau Selection

Evaluate providers on these criteria:

- IRS-approved software platforms

- Transmission speed guarantees

- Support availability during tax season

- Pricing structure (per-return vs. volume tiers)

- Security certifications (GLBA compliance)

Request trial access before commitment.

Phase 2: Workflow Configuration

Establish internal procedures:

- Client Intake: Collect documents and create digital file

- Return Preparation: Complete in approved software

- Quality Review: Internal preparer review before upload

- Authorization: Obtain signed Form 8879

- Transmission: Upload to service bureau portal

- Acknowledgment Processing: Download confirmation and store

Document each step in procedure manual for staff training.

Phase 3: Data Security Implementation

Service bureau models require secure file transfer:

- Use encrypted portals for uploads

- Implement multi-factor authentication

- Restrict access by role

- Monitor login activity

- Maintain client data encryption at rest

California practitioners must comply with California Consumer Privacy Act (CCPA) requirements for client data handling.

Phase 4: Compliance Monitoring

Track these metrics:

- Transmission to acknowledgment time

- Rejection rates by error type

- Client authorization turnaround

- Recordkeeping completeness

- Due date adherence

Monthly review identifies process improvements.

California-Specific Considerations

CTEC Registration Requirements

California Tax Education Council (CTEC) regulates tax preparers. Maintain:

- 60-hour qualifying education

- 20 hours annual continuing education

- $5,000 surety bond

- Current registration certificate display

Service bureau partnerships do not exempt preparers from CTEC obligations.

State Return Handling

California Franchise Tax Board (FTB) maintains separate e-file systems. Service bureaus typically handle both federal and state transmission under single workflow. Verify California e-file capability during provider evaluation.

Local Business Licensing

California cities and counties require business licenses. Costs range $50-500 annually depending on location and revenue. Service bureau models do not eliminate local licensing requirements.

Scaling Operations

Capacity Planning

Service bureau models enable linear scaling:

- No software seat limitations

- No server capacity constraints

- No EFIN practitioner limits

- Add preparers without infrastructure investment

Growth occurs through preparer hiring rather than technology upgrades.

Multi-Location Expansion

California practitioners expanding to multiple offices benefit from centralized service bureau access:

- Single portal for all locations

- Consistent quality control

- Centralized compliance monitoring

- Unified client data security

Each location operates under same procedures without duplicating EFIN applications or software licenses.

Seasonal Staffing

Service bureau models support flexible staffing:

- Train seasonal preparers on standard procedures

- Provide portal access without software installation

- Scale transmission capacity automatically

- Pay per-return costs only for actual volume

This flexibility reduces fixed overhead during off-season.

Compliance Maintenance

Annual Requirements

EROs operating through service bureaus maintain these obligations:

- Review Publication 1345 updates annually

- Update data security procedures for new threats

- Train staff on revised IRS procedures

- Test disaster recovery processes

- Conduct internal compliance audits

Service bureau partnerships do not transfer compliance responsibility. Preparers remain accountable for all IRS requirements.

IRS Monitoring

IRS conducts compliance reviews of high-volume EROs. Maintain documentation demonstrating:

- Proper client authorization collection

- Timely transmission practices

- Accurate recordkeeping

- Data security implementation

- Due diligence procedures

Service bureau transmission records support compliance documentation during IRS review.

Risk Management

Implement these controls:

- Professional liability insurance ($1-2 million coverage)

- Cyber liability insurance for data breach protection

- Client engagement letters limiting scope

- Quality review checklists for each return

- Secure document destruction procedures

California practitioners face additional exposure under CCPA for data breach notification requirements.

This framework enables California tax professionals to scale operations immediately without EFIN delays. Service bureau partnerships provide professional infrastructure while maintaining preparer control over client relationships and tax strategy. Implementation requires systematic procedure development and ongoing compliance monitoring. Growth occurs through preparer capacity rather than technology barriers.